Opinion

The UK's critical minerals ambitions will need Cornwall

Critical mineral projects and new extraction technologies could strengthen the UK's resource security, writes CMGA managing director Ola Zawalna.

Main image: Ola Zawalna, Managing Director of the Cornwall Mining & Geo‑Resources Alliance (CMGA).

Background image artwork was generated using input from AI.

Cornwall is entering a new phase in its mining and geo-resources history, defined by emerging extraction technologies, critical minerals development and renewed investment.

Its geology underpins one of Europe’s most concentrated and diverse subsurface opportunity zones, positioning Cornwall as one of the UK’s most significant emerging critical mineral regions.

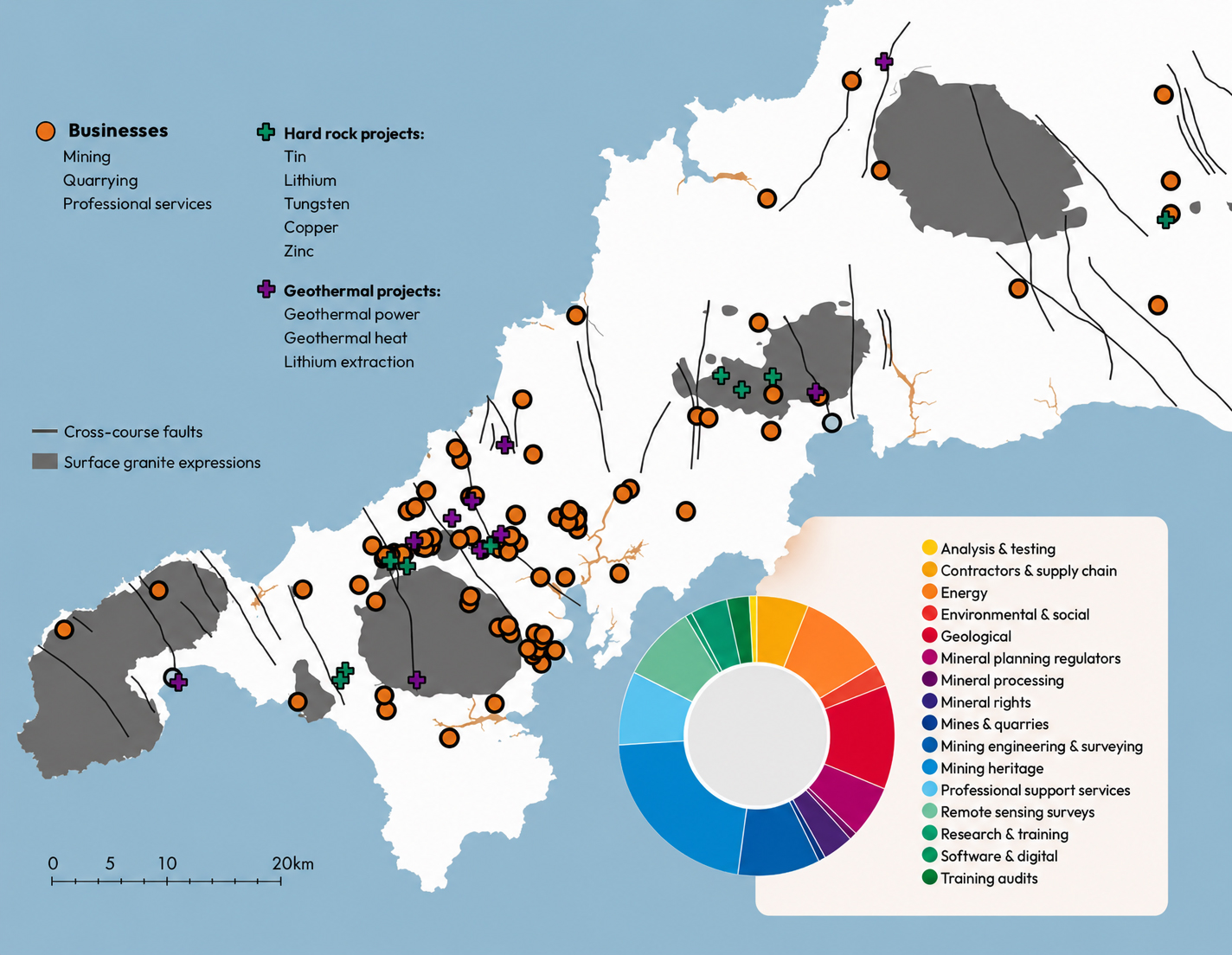

At the centre of this resurgence lies the Cornubian Batholith, a 250km granite body hosting lithium, tin, tungsten, geothermal energy, kaolin and other technology minerals.

Lithium is Cornwall’s most transformative resource; it is essential for lithium ion and emerging solid-state batteries and certain nuclear technologies, but global supply is dominated by China. A domestic UK lithium chain is therefore critical for industrial resilience.

Cornwall's critical minerals projects sit alongside an established mining services network. Source: CMGA

Cornwall has already defined 249.5 million tonnes (mt) of lithium‑bearing hard‑rock resources across two Cornish companies. Cornish Lithium’s project alone contains 183,000t of lithium oxide, and combined, the region could meet the UK’s entire lithium target of around 50,000 tonnes per annum (tpa) by 2035. Cornish Tin & Lithium is also exploring prospects in West Cornwall.

New extraction technologies are central to this progress. Cornish Lithium has built a pilot plant to optimise a full hard‑rock flowsheet using mica‑rich granite, producing battery‑grade lithium hydroxide with UK‑owned processing technology.

Cornwall is also home to advanced geothermal‑brine lithium projects. Geothermal Engineering Limited operates the UK’s first operational geothermal lithium extraction plant, supplied by a 5,275m production well. The lithium extraction facility, sized at 100 tpa, has been installed downstream from the UK's first geothermal power plant, which provides baseload power to the National Grid.

Tin and tungsten are also returning to the UK supply chain. Both are essential for electronics, aerospace, semiconductors, defence, batteries and solar technologies, yet Europe has almost no primary mined tin production and limited tungsten output. China controls most global supply and recent export controls have intensified the need for secure alternatives.

Cornwall is responding with projects capable of meaningful impact. South Crofty, operated by Cornish Metals, is targeting nearly 5 ,000tpa of contained tin in concentrate. If the UK establishes domestic midstream refining capacity and South Crofty’s output is processed into metal, this volume will meet current UK tin demand.

The project reopens one of Cornwall’s most historic underground mines, supported by an 8.5mt resource of which 6mt contains 87.8kt of tin. Mine development is underway, with first production expected in 2028, supported by existing infrastructure and underground workings. Additional tin potential exists at Cornish Metals’ other mineral rights as well as co-products at Cornwall Resources’ Redmoor project and Tungsten West’s Hemerdon Mine, with several early‑stage companies seeking to define tin targets, including Cornish Tin and Tamar Minerals.

Redmoor contains Europe’s highest grade underdeveloped tungsten resources with 85,800t of contained tungsten trioxide, while Hemerdon, the second-largest tungsten resource globally, holds 141,400t of tungsten trioxide within a 113mt combined reserve. If both enter production, the UK could supply around 5% of global tungsten and one‑third of non‑Chinese output. Tungsten West has recommissioned its processing plant and completed successful trials, demonstrating near‑term delivery potential.

Ola Zawalna, Managing Director of the Cornwall Mining & Geo-Resources Alliance (CMGA)

If both [Redmoor and Hemerdon] enter production, the UK could supply around 5% of global tungsten and one‑third of non‑Chinese output.

Click to edit...

Cornwall's mineral potential extends beyond the headline metals. Nickel, cobalt, antimony, lead, gold and zinc remain underexplored, while established operations such as Imerys' kaolin business highlight the region's broader mining and minerals base.

Circular‑economy principles are increasingly embedded across Cornwall’s geo‑resources sector, including the recovery of critical minerals from mine waste and tailings.

Geothermal energy is another defining asset. Geothermal resources can support low-carbon mineral extraction and processing, strengthening Cornwall's credentials as a future critical minerals hub. Combined with Cornwall’s offshore renewable capability, the region is positioned to host some of Europe’s lowest‑carbon mining operations.

The resurgence is rebuilding technical capability through partnerships with the Camborne School of Mines and the wider regional supply chain, with the Cornwall Mining and Geo‑Resources Alliance (CMGA) playing a coordinating role across the industrial ecosystem.

This is not a return to the past, but a technologically driven, environmental, social and governance-led and community-centred pivot to the future. With significant critical mineral resources, emerging extraction technologies and an established industrial base, Cornwall is positioning itself to play a central role in delivering the UK's Vision 2035 Critical Minerals Strategy.