Feature

How DLE is turning oilfield wastewater into a lithium source

Operators across industries are turning to DLE technologies and subterranean brine to get more lithium, faster. Eve Thomas reports.

Main video credit: SmyrnaStok / Shutterstock.com

Lithium demand is set to grow four times by 2035, but the establishment of new projects for traditional lithium mining is slow and capital-intensive. The industry can’t scale up fast enough and the growing gap is revealing a demand for innovative extraction methods.

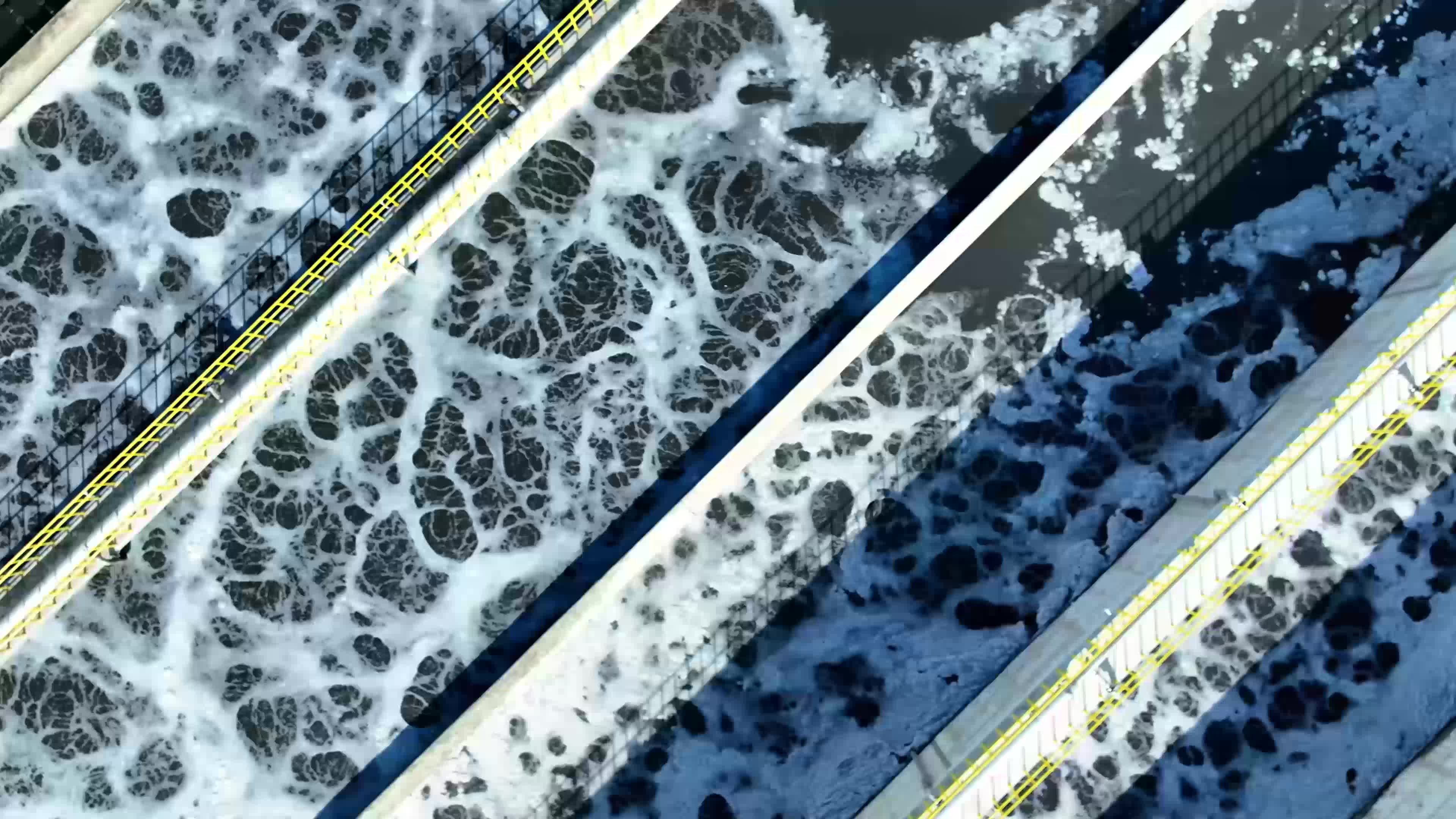

This is where unconventional sources come in: seawater, geothermal brines and oilfield wastewater contain varying but not insignificant quantities of lithium. Evaporation ponds have been used to extract lithium from these brines for almost a century, but the process is slow, typically taking 12–18 months.

However, soaring lithium demand means the race is on to secure supplies.

Direct lithium extraction (DLE) technologies separate lithium from brines in hours or days, offering faster production timelines and, for some operators, a new revenue stream. In the case of oil and gas majors such as Chevron, Equinor and SLB, DLE is an opportunity to monetise wastewater streams. For geothermal players, it is an integrable step before necessary reinjection.

According to some estimates, wastewater produced from Pennsylvania’s Marcellus Shale operations alone could theoretically meet 38–40% of US lithium demand. While this assumes an unrealistic 100% yield, the scale of the opportunity is significant.

“In principle there is no limit to this opportunity,” Paw Juul, chief operating officer at Lithium Harvest, tells Mining Technology. However, there is one major pain point: “It costs significant amounts of money.”

DLE technologies

There are two primary DLE methods applied to lithium-containing brines: solvent extraction and ion adsorption or exchange. The former is a liquid-to-liquid transfer in which the brine is run over a specialised organic solvent and extractant; the second is a liquid-to-solid transfer in which lithium ions bind to the surface of lithium-selective sorbents.

Solvent extraction

Research assistant at the University of Connecticut Hasan Nikkhah explains solvent extraction: “Brine encounters the organic solvent, and the lithium is transferred to it from the brine. Subsequently, we strip the organic solvent and extract lithium from it.”

The organic solvent contains selective extractant, which will interact with the lithium over other materials dissolved in the brine. Once the lithium moves into the organic phase, the product is ‘scrubbed’ (purified) to improve purity and stripped. The organic phase can be regenerated and recycled.

Ion adsorption/exchange

Of adsorption, Nikkhah explains: “In adsorption, we use solid materials to capture lithium from the brine for the adsorption, and after we capture that lithium, we regenerate the material (the solvent to extract that lithium).”

In the DLE process, the brine flows over the solid materials, which are usually resin, or aluminium or magnesium-based materials with active sites on which lithium will interact and be adsorbed. Once the material approaches capacity, the process moves onto the desorption stage: the material is run through either fresh water, or a chemical or acid solution, where it regenerates and releases the lithium in a more concentrated solution, which is recovered for further refining.

Nikkhah notes that the process is essentially the same for ion exchange – they share common design concepts and operating cycles, but ions are exchanged, rather than transferred. While in adsorption the transfer occurs as weak physical forces stick uncharged or charged molecules onto a surface; in ion exchange, a chemical reaction occurs and ions swap to maintain electrical charge balance.

Traditional lithium mining has involved the use of evaporation ponds to extract lithium from brines, but the process is slow, typically taking 12–18 months. Credit: Cavan-Images / Shutterstock.com

A developing area: membrane technology

A developing but decidedly nascent area of interest for DLE is membrane technology, which acts as a selective filter to concentrate lithium ions from brines. There are two primary categories of membrane processes: high pressure-assisted membranes and potential-assisted membrane processes.

The former includes microfiltration, ultrafiltration, nanofiltration and reverse osmosis (all of which feature at some stage in adsorption processes already), while the latter includes electrodialysis, bipolar and capacitive deionisation.

Dr Burcu Beykal, assistant professor of chemical and biomolecular engineering at the University of Connecticut, states that “membrane technology could make a huge difference in terms of like cost effectiveness”, although she adds that “the technology is not quite there yet”.

Costs, waste and environmental profiles: the relative advantages and disadvantages of DLE methods

Solvent extraction and ion adsorption or exchange are currently the two primary processes used for DLE, while membrane technologies are emerging as a potential third. However, Nikkhah notes that there are “also electrochemical methods and chemical precipitation” that can be used. Electrolysis is one area of particular interest as it would drastically reduce the need for chemical reagents; however, research remains at laboratory scale.

Current forays into commercial deployment use ion adsorption. This includes the US’ first lithium extraction plant, which opened in February and is operated by Element3 in the Permian Basin. The second plant, operated by Gradiant, will open later this year in the Marcellus Shale, and will also use ion adsorption.

Significant in both of these cases is the leveraging of existing oil and gas infrastructure to turn industrial waste into a high-value resource. The portfolio diversification brings additional profit, while the potential for on-site processing keeps transport and other operating costs (opex) low.

Juul explains that Lithium Harvest also uses only ion adsorption, noting the environmental shortfalls of the alternatives. “Our technologies need to be as sustainable as possible. Solvent extraction, ion exchange and electrolysis all use a high amount of chemicals and energy,” he says.

High chemical and energy use drives up opex and presents economic ramifications that usually position ion adsorption as the most commercially justifiable DLE technology, although solvent extraction can be more cost-effective for highly concentrated streams. Ion adsorption also uses fresh water for desorption, minimising the need for strong acids and further improving the cost and environmental profile of the method.

However, that is not to say that other techniques lack merit. Ion exchange offers broader opportunities by extracting lithium from much more dilute or lower-grade brines than adsorption. Although the use of chemical stripping generates questions around opex and environmental ramifications, it also means that ion exchange produces more highly concentrated lithium solutions directly than adsorption.

Meanwhile, solvent extraction offers the advantage of efficient distinguishing between similarly sized ions such as lithium and sodium, and builds on established processes already used by mining operators, particularly for copper and uranium.

If membrane technology makes it to commercial scale, it could prove to be the most promising of all: it has the potential to significantly reduce water consumption, land footprint and chemical use, as well as produce a high level of purity, reaching battery-grade.

The oil and gas opportunity

The use of produced water as a feedstock offers a secondary revenue for oil and gas operators, offering two major advantages: portfolio diversification and integration into ongoing operations.

The opportunity has huge scaling potential too – produced water is the largest waste stream associated with oil and gas operations, and wastewater from operations in the Permian basin alone amounts to 22 million barrels every day.

Thus, the lithium opportunity is new not because of the brine resource itself, but the deployment of DLE. Justin Mackey, vice president at REEgen (and previously a researcher at the National Energy Technology Laboratory), explains: “The sheer volume of fluids and the constraints on space in domestic oil and gas operations makes evaporation ponds unfeasible. Now, DLE technologies are trying to basically shrink those operations into modular units.”

Operators have begun to make early moves, and a report by associate professor at Edith Cowan University Amir Razmjou notes that: “The next wave of investments appears to be coming primarily from the oil and gas industry, including companies such as ExxonMobil, Koch Industries, Occidental Petroleum, SLB (formerly Schlumberger) and Chevron Corp.”

Occidental Petroleum and a unit of Berkshire Hathaway formed a joint venture (JV) in June 2024 to produce battery-grade lithium from the brine of ten geothermal power plants in California. Meanwhile, Equinor holds a 45% stake in two of Standard Lithium’s DLE projects located in the Smackover Formation, and Chevron is active in DLE projects in the same region, having acquired two leasehold acreage positions across north-east Texas and south-west Arkansas in 2025.

In the case of oil and gas majors such as Chevron, Equinor and SLB, direct lithium extraction is an opportunity to monetise wastewater streams.

To reach large-scale deployment, however, there are cost bottlenecks. Beykal acknowledges that “produced water is great […] operators can diversify their revenue streams, and they already have to treat produced water”, but she caveats that “you have to consider the operating costs and the disposal conditions that come with it”.

Transporting massive quantities of produced water from oil and gas sites to treatment plants is one notable, significant financial strain. While commercial-scale DLE remains nascent, the necessary infrastructure is lacking to move the lithium-rich brine from the site to the plant. This means that brine is often transported in trucks, representing a considerable cost.

Juul points to the example of the Smackover – an aquifer historically known for rich oil, gas and bromine – which is now one of North America’s most promising, high-grade lithium brine resources. “You cannot pump that much from one place, so you need a lot of infrastructure pipelines. It is a nightmare and it is very costly.”

Considering the US specifically, Mackey concurs: “The regulatory environment for establishing the transportation network needed is limited, and so operators are just trucking [the produced water], and so trucking costs are probably the major cost driver.”

Beykal also notes the financial considerations around DLE, noting that environmental considerations are also reflected on balance sheets. Organic solvents used in solvent extraction are harmful to the environment; even the comparatively cleaner adsorption method has a massive water footprint. “Costs will always be the major driving force, but if you are operating in an area that has high environmental regulations, those waste treatment items can really start piling up your tab,” she says.

How miners are preparing to capitalise

Oil and gas is not the only industry well-positioned to take advantage of the opportunity. Mining operators (some of whom have long been producing lithium via evaporation ponds) are too.

Much of the activity by mining companies is currently centred in South America, home to the ‘Lithium Triangle’ and the world’s largest salt flats.

Codelco and SQM formed a JV (NovaAndino Litio) in December 2025 to develop lithium in the Salar de Atacama until 2060. Over the border, Rio Tinto is developing DLE projects in Argentina, including the Rincon expansion in Salta province, the Sal de Vida project and the Fénix facility in Catamarca province. Eramet is also active in DLE in Argentina.

There are also a growing number of private sector lithium-focused companies exploring DLE as a mining technology. Controlled Thermal Resources uses DLE at its Hell’s Kitchen geothermal project in California’s Imperial Valley, while EnergySource Minerals is preparing to commence project ATLiS in 2028, which will extract battery-grade lithium hydroxide directly from geothermal brines, while also co-producing manganese and zinc.

DLE for oilfield brines could redefine the waste stream as a valuable lithium resource. Credit: alexgo.photography / Shutterstock.com

The production of other minerals from brines via solvent extraction, ion adsorption or exchange is another potentially lucrative direction for interested mining operators.

In fact, Mackey suggests that it is not just about opportunity but commercial viability: “You need to find a market for everything that is in a barrel of water, and there is generally. That is really the path to economic viability – thinking of the brine as a holistic, combined commodity resource.”

Different brines have different makeups, but opportunities include magnesium and rare earths – critical minerals seeing increasing demand as the energy transition picks up pace.

In many brines, vanadium – a malleable transition metal used in grid-scale energy storage – is also present and extractable, as is strontium (famous for use in fireworks but also used in carbonate form in the manufacturing of ferrite magnets for electric motors). In some locations, gold and copper are also present.

“There are many different levels of techno-economic analyses to actually determine profitability”, concludes Mackey. “At the end of the day, all of this water has to be treated and disposed of, and so why not develop this sort of circular solution that also solves another problem?”

Title

With diesel vehicles accounting for 30% to 50% of greenhouse emissions at a mine site, replacing them with a battery-electric fleet is a sure way to drastically reduce overall CO2 emissions, but how else can mines benefit from this technology?

Leading underground manufacturers Normet believe the answer lies with SmartDrive. This architecture for battery electric vehicles (BEV) was developed in collaboration with customers, building on feedback, predicting future trends, and assessing the limitations of diesel engines, and comes with a wealth of benefits for operators.

Title

TowHaul Lowboys are front loading which is crucial for three main reasons:

Speed – the Gooseneck can connect and disconnect in as little as 90 seconds

Safety – the full width of the lowboy rests on the ground providing a wide, stable loading platform

Versatility – the multi-purpose gooseneck can be used to tow disabled haul trucks or other specialty TowHaul trailers (Dragline Bucket Transporter or Water Tank Carrier)

The “Low-Profile” designation refers to the load ramps of the lowboy which are designed in such a way as to reduce the “breakover” as the equipment transitions from the ramps to the lowboy deck.

The “Modular” aspect refers to how the lowboys are designed, manufactured and shipped. Each module is easier to handle and ship which substantially lowers shipping costs for our clients, especially those overseas. Once onsite, the modules are pinned together which minimizes installation time (3-5 days).

TowHaul Lowboys utilize a single, haul-truck type axle. TowHaul offers a dry drum brake configuration or a wet brake configuration with TowHaul’s patented Brake Cooling System.

Frank Smith, Founder and CEO of TowHaul

TowHaul Lowboys utilize a single, haul-truck type axle. TowHaul offers a dry drum brake configuration or a wet brake configuration with TowHaul’s patented Brake Cooling System. Using a single axle eliminates tire “skidding” often found with multi-axle trailers when turning on a sharp corner. This “skidding” can cause tire and axle damage leading to downtime. Recognizing the variety of conditions in which mines operate, TowHaul has designed specific lowboy configurations tailored to operate more effectively in specific areas. For example, there are several TowHaul Lowboys currently operating in the unique conditions found in the oil sands of northern Alberta designed with a specific Oil Sands Configuration.

To cope with the extreme ambient temperatures found in Western Australia, TowHaul upgraded the patented Brake Cooling System for our 450-ton capacity lowboys to improve the cooling of the oil in those systems.

Mining industry needs clarity

Macfarlane has been critical of taxation policy in the past, branding it a ‘threat’ to mining in and suggesting it puts the local sector at a disadvantage compared with other regional sectors across the country.

“Coal royalties in Queensland are the highest in the country and more than double the rate of New South Wales. Latest figures show the resources industry is delivering A$5.2bn to the State Budget in royalty taxes, including A$4.36bn from coal. These are record returns and they show the importance of the resources sector to the state budget. We have asked for certainty about royalty tax rates to ensure stability for long-term investments and the jobs they create.”

In early June 2019, mining companies avoided increases to royalties by agreeing to provide A$70m to a A$100m infrastructure fund.

Frank Smith, Founder and CEO of TowHaul

In early June 2019, ahead of Queensland’s State Treasurer Jackie Trad’s budget, mining companies avoided increases to royalties by agreeing to provide A$70m to a A$100m infrastructure fund. The move means coal royalties will be frozen for three years.

“We have welcomed the commitment from the Queensland Opposition to freeze royalty tax rates for 10 years, and we’d like to see a similar commitment from the Government,” says Macfarlane. “We want to keep employing more Queenslanders and supporting more regional communities through local investment. To do that, it’s essential that we have clear and transparent rules and regulations,” he adds.

Will politics continue to support mining?

Politics and mining often overlap - unsurprisingly given the value of the sector to the wider Australian economy. That was on display during the recent federal election, which saw the industry used as a political tool– particularly Adini’s controversial Carmichael coal mine in the Galilee Basin.

However, the re-election of Scott Morrison as prime minister was welcomed by many within mining, and the almost complete annihilation of Labor’s vote in the state sent a clear message to politicians about how Queenslanders view the sector. Before the election Labor had failed to take a meaningful position on the project but appeared likely to oppose it. The party suffered heavy losses, hampering its ability to have a significant say at a state level. Olive Downs is a case in point, just days after the vote Queensland’s government gave final approval to the project, which had been stuck for years.

Keen to stress the need for a broad political approach to mining, Macfarlane says: “The QRC works with all sides of politics constructively, including the re-elected Coalition Government in Canberra. The Government has been a strong supporter of the resources sector through the Prime Minister and Resources Minister Matt Canavan.

Phillip Day. Credit: Scotgold Resources

“The resources industry has also welcomed the appointment of Joel Fitzgibbon to the shadow resources portfolio. We want to see bipartisan support for the resources sector and the regional jobs it creates. We want to see the Government and the Parliament focus on attracting new investment to create new jobs well into the future.”

Queensland’s mining industry is a vital part of the economy and has a promising future. However, nothing can be taken for granted and business, politicians, and local communities need to be ahead of the issues the future may bring MacfarlaneWe must embrace technology to stay globally competitive, compete for every contract and earn the support of our governments and the people who elect them. believes.

“Our sector makes up almost 20% of the Queensland economy but we must not get complacent. We must embrace technology to stay globally competitive, compete for every contract and earn the support of our governments and the people who elect them,” he finishes.